SABEENA BUBBER

MORTGAGE BROKER | AMP

Hello, I’m Sabeena Bubber, thanks for taking the time to visit my website. I’m a mortgage consultant with Xeva Mortgage.

I am committed to finding solutions for my clients that go beyond just getting a good interest rate. I am a specialist in reading fine print and love to help my clients get the mortgage product that best suits their needs. Just a reminder that as your mortgage broker I work for you, not for the bank. I have access to multiple products and solutions and I am committed to finding the mortgage that is right for you. I believe in establishing long term relationships with my clients. I am more than happy to help you secure a single mortgage, but I get really excited about giving you mortgage advice for life!

My clients know that I have their back, I do annual reviews and advise my clients when they are paying too much for their mortgages (when was the last time your bank called you to tell you that you are paying too much and they can save you money?). As such, my clients come back to me for advice frequently during the mortgage term so that we can align their mortgage repayment strategy with their other financial goals.

NEL C

Happy Client

Sabeena assisted us with refinancing and renewing our mortgage. We felt she made it a priority to ensure our financial goals are reached. She was attentive to our needs and timeline and an absolute pleasure to work with. We highly recommend her services.

My Process is Simple

STEP ONE

Start the conversation.

The best place to start is to connect with me directly. The mortgage process is personal, and it can be daunting. My commitment to you is that I'll listen to all your needs, assess your financial situation, and provide you with a plan to move forward.

STEP TWO

Discover the best option.

Once we’ve had a look at your financial situation, we’ll consider a variety of mortgage options, I’ll outline what documents are necessary to qualify for a mortgage, negotiate with the lenders on your behalf, and arrange the mortgage that best suits your needs.

STEP THREE

Sit back and relax.

Once we’ve arranged the mortgage product that best suits your needs, you’re not alone. I’m your mortgage professional for life. If you’ve got questions in the years to come, I’m always available to make sure that your mortgage is working FOR you, and not the other way around!

Videos

Visit my videos page for more helpful information.

Podcasts

Features

Nice Things My Clients Say

Getting a mortgage shouldn't be confusing. I'll guide you through it.

Mortgage Services

Know the right mortgage product for your circumstance.

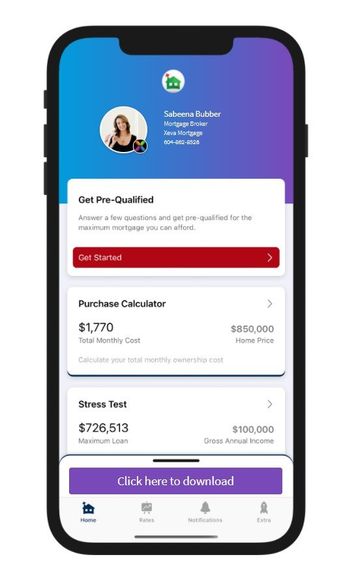

Download my Mortgage Toolbox

- Calculate your total cost of owning a home

- Estimate the minimum down payment you need

- Calculate Land transfer taxes and the available rebates

- Calculate the maximum loan you can borrow

- Stress test your mortgage

- Estimate your Closing costs

- Compare your options side by side

- Search for the best mortgage rates

- Email Summary reports (PDF)

- Use my app in English, French, Spanish, Hindi and Chinese

Looking to run some numbers?

If you're going through a divorce

and need mortgage advice.

You don't have to suffer in private,

you're not alone on this journey.

Visit my dedicated site for those navigating separation and divorce.

Access free resources and expert guidance to help you through this transition.

55+ and looking for solutions to enhance your lifestyle?

Would you rather just get down to it and have me tell you exactly how much you qualify for?

Articles

I keep my Articles up to date so you can stay informed.

LET'S TALK